NEW YORK (CNNMoney.com) -- When the Federal Reserve's policy-making committee meets Tuesday, there will be no mystery as to what they will do. Nothing.

But what will the Fed say? That's where things get interesting.

|

| Click the chart to keep track of other rising commodity prices |

In the past few weeks, fears of a double-dip recession have ebbed. August retail sales were better than expected. The number of people filing for unemployment claims has fallen for two weeks in a row.

The trade deficit for July was much narrower than forecasts. That's crucial since a ballooning trade gap in June was the primary reason why the nation's gross domestic product in the second quarter was revised lower.

Still, the economy is not healthy. The latest bits of manufacturing data have been disappointing. The housing market may not have hit bottom yet. Builder Beazer Homes USA (BZH) lowered its forecast for new home orders on Wednesday.

And even with jobless claims falling, companies don't seem to be comfortable enough to start hiring again. Some are still getting rid of workers. FedEx (FDX, Fortune 500) said Thursday it was cutting 1,700 jobs.

For these reasons, the Fed is likely to stress -- as it has since March 2009 -- that it expects to keep interest rates "exceptionally low" for "an extended period of time." (Rates have been near 0% since December 2008.)

It may also talk more about its commitment to purchase long-term bonds as it sees fit. In its last meeting, the Fed said it would reinvest the principal from mortgage-backed securities it holds into long-term Treasurys.

But it stopped short of announcing a new plan to buy bonds, a practice known as quantitative easing.

David Joy, chief market strategist with Columbia Management in Boston, said the economy doesn't appear to be so weak that the Fed should step up its bond buying yet. But it can't afford to be complacent either.

"The message we are left with from all the recent data is that this is a sluggish recovery," Joy said. "The Fed may feel a little better about the economy since they last met in August -- but not much."

But if the economy takes a sudden turn for the worse again -- Jon Stewart recently joked that "the 'Summer of Recovery' is quickly sliding into the 'Autumn of Nothing but Ramen Noodles For Dinner,' " -- then the Fed will have to give specifics about its plans to buy more bonds.

"The Fed may have to be aggressive," said Anthony Valeri, market strategist with LPL Financial in San Diego. "What people are looking for is a dollar amount. It could be $500 billion to $1 trillion."

Valeri doubted the Fed would make such an announcement on Tuesday but said it was possible it would unveil more concrete plans at its November 3 meeting.

Still, some think the Fed may have to think more about pulling back on its easy money policies. That's because there are still niggling worries about inflation.

Yes, inflation.

Deflation may be the big buzz word as economists fret about whether the United States is heading for its own version of Japan's Lost Decade during the 1990's.

But have you looked at what commodity prices are doing? The Fed may soon need to start worrying about that dreaded 1970's throwback of stagflation: the combination of anemic growth and rising prices.

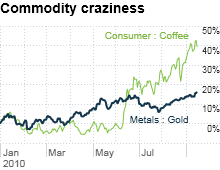

Gold is hitting record highs. Agricultural commodities are soaring and in some cases, such as bacon and coffee, producers are passing higher costs onto consumers. And the dollar has been on a downward slide against the yen and euro.

While it would be foolish to suggest that the spike in commodities is entirely the Fed's fault, it is fair to say the central bank's more pessimistic take on the economy sparked worries that the Fed will be too slow to react to pricing pressures.

"The Fed may have jumped the gun last time and created the fear that things are worse then they actually believed," said Milton Ezrati, senior economist with Lord Abbett, an investment firm in Jersey City, N.J.

Ezrati said the increase in commodity prices is evidence that deflation and double-dip talk may be overblown. Along those lines, the latest figures on inflation on a wholesale level, the producer price index, rose more than expected in August. Consumer prices also were up a bit more than forecasts in August.

And even though the so-called core PPI number, which excludes food and energy costs, was in line with forecasts, the myopic focus on that number is sometimes silly.

People have to eat and drive. If fuel and food costs keep going up, try telling consumers they need to worry about deflation.

"You would think the Fed should mention the risk that commodity prices could go higher," said Andrew Busch, global currency and public policy strategist with BMO Capital Markets in Chicago. "The Fed needs to discuss the potential for inflation for the long term."

- The opinions expressed in this commentary are solely those of Paul R. La Monica. Other than Time Warner, the parent of CNNMoney.com, and Abbott Laboratories, La Monica does not own positions in any individual stocks. ![]()

No comments:

Post a Comment